04 Apr 2026 | How ITR and CIBIL Score Affect Education Loan for Study Abroad

0

8

Introduction

Having more than 15 years of experience advising students on international admissions and financial planning, I have observed one common mistake: students study IELTS and SOPs but pay no attention to their CIBIL education loan score and financial documents. They later discovered that when they go through the process of availing the study abroad loan, admission does not necessarily mean that you are funded.

The Ministry of External Affairs stated that there were over 13 lakh Indian students abroad in 2023 (MEA Data). At the same time, according to the RBI, there is a positive trend in student loan disbursements in India, indicating that more people are relying on bank funds. This renders it absolutely necessary to learn about the education loan CIBIL score, ITR for education loans, and the general study abroad loan process.

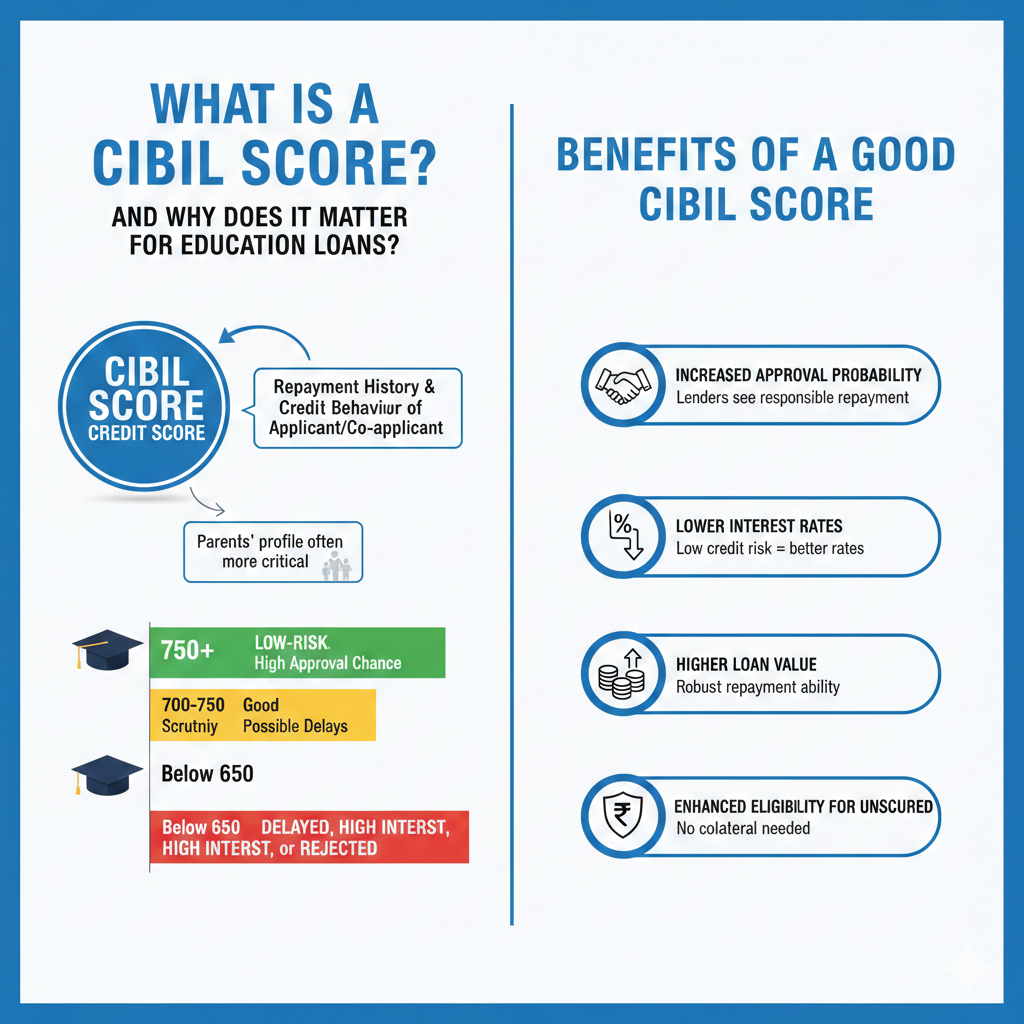

What is a CIBIL Score and Why Does It Matter for Education Loans?

The CIBIL score for an education loan is a three-digit credit score that indicates the repayment history and credit behaviour of the loan applicant or co-applicant. Mostly, banks consider the parents' profile more critical.

From my professional experience:

- A score of 750 and above goes a long way in supporting your application to borrow, since that is a signal that you are a low-risk borrower.

- A score of 700-750 can still be counted, but banks may be more stringent in scrutinising the study abroad loan process.

- Student loans in India are likely to get delayed, charged higher interest, or rejected if the score is below 650.

An education loan with a good CIBIL score assists in the following ways:

- It increases the probability of loan applications due to lenders' history of responsible repayment.

- It also lowers interest rates because when credit risk is low, banks can offer lower rates.

- It enhances the approved loan value in the study abroad loan process, as repayment ability appears more robust.

- It enhances eligibility for unsecured student loans in India, where there is no collateral requirement.

I had recently dealt with a student at Jaipur who had been accepted into a university in the UK. The unsecured loan was approved within 7 working days, indicating that his father had a CIBIL score of 782 in his education loan application. However, the situation is different with another student with a score of 648, who had to undergo three stages of clarification during the study abroad loan process.

Role of ITR for Education Loan Approval

The education loan CIBIL score indicates credit discipline, whereas the ITR for the loan indicates a stable income.

Banking institutions are known to take 2-3 years of ITR to confirm stable incomes. Right ITRs in the case of education loan documentation provide lenders with assurance that the EMI is within the borrower's financial capability.

Key aspects banks evaluate:

- Stability of income, since an unstable income may undermine the study abroad loan process.

- Announced income per year, which directly influences the maximum amount of loans to which the applicant is eligible under the student loans in India.

- Tax compliance issues, such as non-filing or irregular filing of reports, raise red flags in ITRs for education loans.

During my 15+ years of consulting experience, I have encountered scenarios where strong academic records did not matter because of poor ITRs in education loan records. The student who was targeting Canada had a co-applicant with a high monthly income but had not filed ITR regularly, which delayed the study abroad loan process by more than a month.

In simple terms, a clean ITR for an education loan has the same weight as a strong education loan CIBIL score in terms of financial credibility.

How Banks Evaluate Your Profile in the Study Abroad Loan Process?

The loan process for studying abroad is systematic but risky. There are various parameters that banks put together to approve funds.

Step-by-Step Evaluation

- Admission Verification ensures that the university and course meet the eligibility criteria for student loans in India.

- Financial Document Review involves evaluating the ITR for education loans and salary documents to assess repayment strength.

- The Education Loan CIBIL Score Check helps lenders gauge past and future behaviour.

- Liability Assessment computes current EMIs to provide a glimpse of the financial responsibility associated with the study abroad loan process.

- Final Risk Scoring is a composite of all financial parameters before the loan is sanctioned.

How CIBIL and ITR Work Together?

|

Factor |

What It Shows |

Impact on Study Abroad Loan Process |

|

Education Loan CIBIL Score |

Credit repayment behavior |

Influences approval speed & interest rate |

|

ITR for Education Loan |

Income stability & tax compliance |

Determines eligible loan amount |

|

Existing Liabilities |

Debt burden |

Affects EMI eligibility under student loans India |

A weak education loan CIBIL score without an appropriate ITR can result in a smaller loan amount. On the same note, achieving a good credit history may be difficult for high-income individuals.

Impact on Secured Vs Unsecured Student Loans in India

When planning finances, it is important to understand the type of loan you are taking.

Secured Loans

- The middle level of education loan CIBIL score can still be accepted as collateral, which minimises lender risk.

- Simple compliance with ITR requirements regarding education loans is required to determine repayment capability.

- The property valuation can delay the application process for study abroad loans.

Unsecured Loans

- A CIBIL score is mandatory for higher education loans, as there is no collateral to support the loan.

- A good, steady ITR for education loans is crucial for risk assessment.

- Combined financial strength is critical for student loan approval in India.

The success rate of most of the unsecured approvals I secured in my consulting business is highest when I have a good education loan CIBIL score and an ITR education loan.

Common Reasons for Education Loan Rejection

Based on real case analysis, some of the most frequent reasons for rejection are:

- Poor education loan, CIBIL score and this is an indicator of high credit risk to the banks.

- Independent incomplete ITR of education loan, raising questions about the stability of income.

- Existing liabilities, which are high, have a lower repayment capacity in student loans in India.

- Mistakes in paperwork make the process of obtaining the study abroad loan a waste of time.

These challenges can be avoided through early planning.

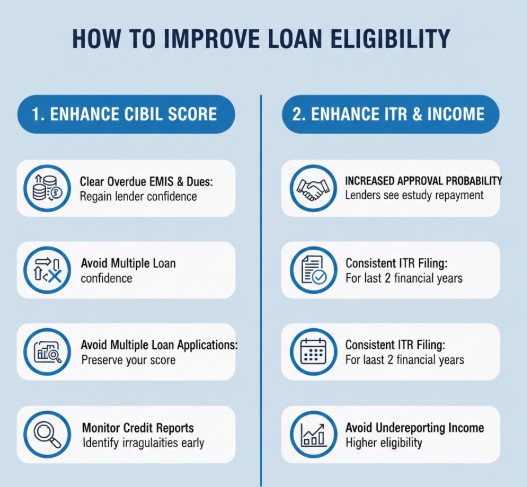

How to Improve Your Loan Eligibility Before Applying?

The strategies I would recommend families to consider before going through the process of study abroad loan include:

Enhance Education Loan CIBIL Score.

- The overdue EMIs and credit card dues have been pending for clearance to regain lenders' confidence.

- Applying for several loans before obtaining education financing is a mistake you should avoid to preserve your education loan CIBIL score.

- Check credit reports regularly to identify irregularities in advance.

Enhance the ITR of the Education loan.

- Filing income tax returns- Filing income tax returns should be done consistently over at least two financial years.

- One should avoid underreporting income because lower reported income means lower eligibility for student loans in India.

Ensure that financial records are maintained at a steady level to enhance confidence in the loan process for studying abroad.

Final Thoughts from My Experience

I have been helping hundreds of families over the years go through complex funding journeys. The biggest lesson I have for all learners is that your education loan CIBIL score and your ITR for education loans are as important as your university invitation letter.

Interest rates and approval times are reduced when interest rates are favourable, and the process of applying for the study abroad loan is hassle-free in India.

Planning is the key to financial planning. The CIBIL score for an education loan should be reviewed, the ITR should be clean to provide education loan details, and the process of applying to study abroad should be carefully considered and not done on a whim.

For more assistance please visit us study abroad consultancy, and avail of our wide range of services for students on destinations like study in USA, study in UK, study in Canada, study in Australia, study in ireland and many more country.

FAQs

What is the lowest required CIBIL score in case of an education loan?

For student loans in India, an education loan, a CIBIL score of 700 or above is usually required to obtain a study abroad loan.

Is it mandatory to have ITR loan education?

Yes, an ITR is normally required to demonstrate a stable income during the loan process when studying abroad.

Is it possible to get a student loan in India with a low CIBIL education loan score?

Yes, although consent can be hard or more expensive, particularly in unsecured situations, in the process of a study abroad loan.

What will be the number of years of the ITR of the education loan?

Education loans require 2-3 years of ITRs, as most banks use them to assess repayment capacity.

Is there a significance to the education loan CIBIL score and ITR?

Yes, education loan, CIBIL score and ITR education loan make a joint decision on whether it is approved under student loans India, and they affect the study abroad loan process.

Author Bio

Abhinav Jain - Founder, Gateway Educonnect and Director.

B.Tech, MBA, AI and Global Education Specialist.

More than 15 years of professional experience in leading students along international routes based on politics and innovation.